Glossary of Terms

| Cost of Goods Sold (COGS) | Cost of goods sold refers to the direct costs of producing a product or service. COGS includes direct labor costs (internal employees only), materials, and trade partners (subcontractors hired to perform work who often supply their own materials and labor). COGS are subtracted from a company's revenue to determine its gross profit. |

|---|---|

| Overhead |

Overhead refers to costs associated with running a business, including administrative labor, owner compensation, software subscriptions, office expenses, etc. Indirect expenses are typically subtracted from the gross profit to arrive at net profit. Overhead is comprised of fixed and variable costs: Fixed Costs – Refer to indirect costs that are the same amount every month or year, such as your vehicle payment, office lease, or software subscription. Variable Costs – Refer to indirect costs that might fluctuate each month or year such as fuel, utility payments, and credit card payment fees. |

| Contract types |

Cost plus – In a cost-plus contract, the client agrees to reimburse a contractor for the cost of goods expenses such as labor, materials and trade partners incurred in completing a project, plus an additional fee typically representing the contractor's contribution to overhead and profit. The cost-plus contract is often used for complex projects in which many details are unknown prior to the start of the project. It offers higher transparency to the client and balances the risk between the contractor and the client. Fixed cost – A fixed-cost contract is an agreement in which a contractor is paid a set amount for a specific scope of work (SOW) regardless of the actual costs incurred during the project. Estimates and invoices are shared as a lump-sum price that does not include a breakdown of project components. This type of contract provides the lowest amount of transparency to the client and places the risk on the contractor, who must complete the project within the agreed budget and timeframe to ensure profitability. It is typically used when project details are clear and predictable, allowing for accurate cost estimation. Fixed-cost contracts are favored by clients who want to avoid unexpected cost overruns, as they provide certainty on the maximum amount payable for the project. |

| Markup |

Markup is the amount added to COGS to determine the price and is expressed in a percentage. It is typically used to ensure that the price set for a product or service covers the cost of producing it and includes a contribution to overhead and net profit. For example, if a product costs $1.00 and is marked up to sell for $1.50, the markup is 50%. Markup and margin are not the same. Markup set in Buildwise is used in the Estimate and Change Order builders. With Buildwise, you set a global markup % in your Company Settings. However, you can also set COG-specific markups at a Project level in Project Settings. Refer to the article Set Up Markup Costs. |

| Margin |

Gross profit margin – Refers to the amount of Total Income minus the Total COGs. To represent this as a % (most common), divide the Gross Profit in $ by the Total Income. Gross Profit Margin $ = Total Income - Total COGS Gross Profit Margin % = (Total Income - Total COGS) / Total Income For example, if you sell your product for $1.50 and the product costs $1.00 to build, your gross profit margin is ($1.50 - $1.00) / $1.50 x 100 = 33%. This means you use a 50% markup to achieve a 33% gross profit margin. Net profit margin – Refers to the percentage of total revenue that the company retains after incurring both the direct (COGS) and indirect (Overhead) costs associated with producing the services it provides. It is primarily used in analyzing a company’s profitability. From the above example, let’s say 10% of each $1.00 you invoice goes to your overhead. Then, you would subtract this from the gross profit to come up with your net profit margin. Net Profit Margin $ = Gross Profit Margin - Overhead Net Profit Margin % = (Gross Profit Margin - Overhead) / Revenue |

| Labor burden | Labor burden refers to the direct costs associated with employing labor beyond the workers' hourly wage or salary. It includes expenses such as workers' compensation insurance, health insurance, paid time off (PTO), and retirement benefits. Accurately calculating the labor burden is important for businesses to understand the true cost of employing staff and to price their products or services appropriately. Refer to Team Member Pay and Charge Rates. |

| Pay rates | Pay rates in Buildwise refer to the fully burdened rate you should be using to calculate the gross profit earned on each hour worked by your employees. This is calculated through the Labor Burden worksheet and understanding all of the costs on top of the employee's wage that you, as their employer, are required to pay. Refer to Team Member Pay and Charge Rates. |

| Charge-out rate |

Charge-out rate is the rate a business sets for services or labor billed to clients. This rate is typically calculated to cover the costs of the labor (including wages and labor burden), overhead expenses, and a margin for profit. The charge-out rate is often higher than the actual wage paid to the worker, as it needs to account for the additional costs of running the business and ensure profitability. It is a critical component in service-based industries, as it directly affects revenue and profitability. Charge-out rates have an impact on both cost-plus and fixed-cost projects. In Buildwise, you only need to set the charge rate for cost-plus projects, as the profit calculations are used differently for this type of project. |

|

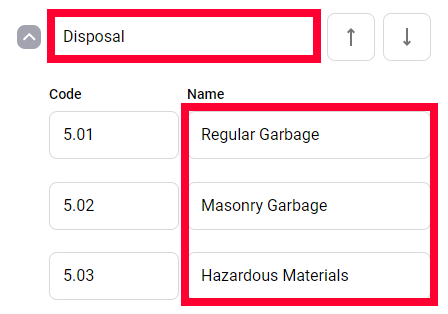

Cost Groups, Cost Items, Cost Sections |

For details, refer to Understanding Cost Groups, Cost Items, and Cost Sections. Cost Group – A cost group is a step in a construction project such as demolition, framing, and drywall. Buildwise uses a simplified set and represents the information across three COGs (labor, material, and trade partners). Cost Items – A cost item is a subtask within a cost group. The example below shows a cost group called Disposal with cost items Regular Garbage, Masonry Garbage, and Hazardous Materials.

In Buildwise, we encourage you to build your estimates and change orders using cost groups and cost items, but for entering expenses and tracking them, we only use cost groups. Cost Sections – A cost section is a way to group scope of work together by a work area within a cost group. Example: The Estimate Builder below shows a cost group of Framing with two cost sections of First Floor and Second Floor and associated cost items nested within them. The cost sections group the different aspects of a framing project by the floor in which it occurs.

|

| Costs |

Estimated costs – Refers to the original calculation of the COGS when building your estimates. The term is used in a comparative method of estimated to actual costs. Actual costs – Refers to the ongoing experienced costs of a project. The term is used in a comparative method of estimated to actual costs. |

| Hours Per Day | Hours Per Day is the number of billable hours your employees work onsite each day and is used to calculate the Remaining (Days) left within a cost group and/or the project as a whole. |

| Remaining (Days) |

Remaining (Days) represents the number of days you have left after dividing Remaining (Hours) by Hours Per Day. Remaining (Days) = ([Estimate Hours + Change Order Hours] - Actual Hours) / Hours Per Day If you have more than one individual planned to be on the project, then divide the Remaining (Days) by the number of team members. Remaining Person Days = Remaining (Days) / # of people on the project |

| Average Estimated Labor | Average Estimated Labor Rate field sets a default labor rate used when creating estimates and change orders. This rate typically factors your labor burden and profit you want to earn for each hour worked. This rate is entered as a default rate in Settings > Preferences; however, it can be changed in-line when creating estimates or change orders. |